The Sector Edge - January 26, 2026

- Stephen Suttmeier

- Jan 26

- 17 min read

*** Please see the bottom of this report for important disclaimers and disclosures.***

|  |

Ranks and scores plus XLF, XLB, XLE, XLU, and XLP

Tactical Ranks: Cyclicals remain in top five as XLK drops into bottom five

The Top Five Tactical Sector Ranks are Materials (XLB), Energy (XLE), Healthcare (XLV), Industrials (XLI), and Discretionary (XLY). XLY replaced Technology (XLK) in the top five. XLB, XLV, and XLI also have top five 52-week Ranks.

The Bottom Five Tactical Sector Ranks are Utilities (XLU), Financials (XLF), Real Estate (XLRE), Comm Services (XLC), and Technology (XLK). XLK replaced Discretionary (XLY) in the bottom five. XLU, XLF, and XLRE also rank in the bottom five of the 52-week Rank, but XLK and XLC hold the top two 52-week Ranks.

Financials: Big drop from early January peak pressures key WMA support zone

Financials (XLF) remain in a positive absolute trend, but the zone of the rising 13-, 26-, and 40-week moving averages (WMAs) from 53.83 to 52.61 is under pressure. If XLF breaks these WMAs, it would expose big support at the August and November 2025 lows near 51. A rally back above 53.83-54.11 (13-WMA and last week’s high) is required to confirm the rising 26- and 40-WMAs from 53.42 to 52.61 as support within an ongoing upward trend. If XLF can defend the low 50s as support, then the mid 2025 breakout that projects XLF to 61.25 remains intact.

Materials: Bullish breakouts point higher toward the 52 and 56 areas

We highlighted the potential for Materials (XLB) to break out above resistance at 46.14-46.43 (61.8% extension and July-September peaks) (December 29, 2025 The Sector Edge). XLB cleared this resistance in early January and pushed to a new all-time high last week. This suggests upside to 51.90-52.07 (converging 100% extensions) and then to 56.30 (late 2024-early 2026 basing pattern count). The immediate trend is bullish above 48 (61.8% extension and last week’s low) with more significant support at the basing pattern breakout zone at 46.43-46.14.

Energy: Bullish breakout intact above 47.41-46.46 and targets 56.75

Our January 5 The Sector Edge highlighted that Energy (XLE) was in position to break higher from a late 2024 into early 2026 bullish consolidation. The rally above 46.46-47.41 confirmed this positive setup to suggest upside potential beyond the 2024 highs at 48.96-49.49, which XLE is testing, to the mid 2024 peak at 50.76 initially and then higher toward the pattern count at 56.75. Prior resistance at 47.41-46.46 reverses its role to support.

Utilities: A challenging setup while below 43.53-43.83

Utilities (XLU) have corrected within an uptrend and have traded between rising 26 and 40-week moving averages (WMAs) since early December. While below 43.53-43.83 (13- and 26-WMAs and chart resistance), the risk is for a head and shoulders top. Key support is 41.70-41.15 (late 2024-mid 2025 base breakout/retest zone). If XLU loses this support, it would confirm the topping pattern with deeper risk to 40.26-39.43 (chart support levels and 38.2% retracement). Until a loss of that support, it would take a rally above 43.53-43.83 to reassert the uptrend for XLU.

Staples: Rallies toward range highs on stealth defensive leadership from October

Staples (XLP) broke above tactical resistance at the declining 26- and 40-week moving averages (WMAs) and chart levels at 79.45-80.25 to confirm an early January weekly bullish engulfing pattern and target the mid 2025-late 2024 peaks at 83.30-84.53 (January 12 The Sector Edge). Prior 80.25-79.45 resistance reverses its role to support. If XLP remains above this support, the potential increases for an upside breakout beyond the 2024-2025 peaks.

Sector Ranks and Scores

S&P 500 GICS Level 1 Sector ETF Ranks and Scores

We evaluate the relative strength and momentum of S&P 500 GICS Level 1 sector ETFs using a multi-dimensional ranking approach. This analysis incorporates both short-term and long-term performance metrics to identify sector leadership and underperformance. Key inputs include Tactical Rank, 52-week Rank, Trend Scores, and Long-term Trend Scores. Trend Scores are evaluated on both an absolute price basis and relative to the S&P 500 (SPX) benchmark. Combined, these indicators provide a comprehensive view of each sector’s technical condition and trend durability across multiple timeframes.

Key Indicators

Tactical Rank: Uses three short- to intermediate-term weekly simple moving averages (WMAs) to determine the rank: The 13-, 26-, and 40-WMAs. Longer WMAs carry greater weight in the ranking.

52-week Rank: Calculated using the 52-week rate of change to assess longer-term strength.

Trend Score: Ranges from -10 to +10 and incorporates the 13-, 26-, and 40-WMAs. Higher scores indicate stronger trends with prices above rising WMAs. Lower scores indicate weaker trends with prices below declining WMAs. Longer WMAs are more heavily weighted.

Trend Score vs. SPX: Applies the same methodology as the Trend Score but uses the ratio of the ETF versus to the S&P 500 Index to determine relative performance.

Long-term Trend Score: Ranges from -20 to +20 and includes the 13-, 26-, 40-, and 200-WMAs. Higher scores reflect stronger long-term uptrends, while lower scores indicate long-term downtrends. Longer WMAs carry more weight.

Long-term Trend Score vs. SPX: Applies the Trend Score LT methodology to the relative price ratio of the ETF compared to the S&P 500.

The rally from the April 2025 low has broadened since late November

Three sectors are beating the S&P 500 (SPX) on the rally from the April 2025 low: Technology, Industrials, and Discretionary. Technology remains the standout winner, while Industrials and Discretionary more recently surpassed the SPX. After a 5%+ pullback from late October into the November 20 low, leadership expanded to seven sectors, with Materials, Consumer Discretionary, Industrials, and Energy posting double-digit gains, while Consumer Staples has also outperformed alongside the growth sectors of Technology and Communication Services. The remaining four sectors remain relative laggards, though Utilities is the only sector showing a negative return since late November.

Chart 1: Sector ETF price returns from the April 2025 low (top) and the late November 2025 low (bottom)

Source: Optuma, Suttmeier Technical Strategies

S&P 500 GICS Level 1: Sector ETF Summary

Top Five Tactical Sector Ranks: XLB, XLE, XLV, XLI, and XLY

The Top Five Tactical Sector Ranks: Materials (XLB), Energy (XLE), Healthcare (XLV), Industrials (XLI), and Discretionary (XLY). XLY replaced Technology (XLK) in the top five. XLB, XLV, and XLI also appear in the top five of the 52-week Ranks. XLB and XLE reached 52-week weekly closing basis highs last week.

Bottom Five Tactical Sector Ranks: XLU, XLF, XLRE, XLC, and XLK

The Bottom Five Tactical Sector Ranks: Utilities (XLU), Financials (XLF), Real Estate (XLRE), Communication Services (XLC), and Technology (XLK). XLK replaced Discretionary (XLY) in the bottom five. XLU, XLF, and XLRE also rank in the bottom five of the 52-week Ranks, but XLK and XLC hold the top two 52-week Ranks.

Tactical Ranks

· Top Five: Materials, Energy, Healthcare, Industrials, and Discretionary

· Bottom Five: Utilities, Financials, Real Estate, Communication Services, and Technology

52-week Ranks

· Top Five: Technology, Communication Services, Industrials, Materials, and Healthcare

· Bottom Five: Real Estate, Financials, Staples, Discretionary, and Utilities

Trend Scores

· Bullish absolute and vs. SPX: Healthcare and Technology

· Bearish absolute and vs. SPX: Real Estate

· Bullish absolute but negative relative scores: XLC, XLU, and XLF

· Zero absolute score: Staples – improved from negative with the potential to shift positive

· Zero relative scores: Industrials, Materials, Energy, and Discretionary – improved from negative with the potential to shift positive

Long-term Trend Scores (LT Trend Score)

· Bullish absolute and vs. SPX: Industrials, Technology, and Communication Services

· Bearish absolute and vs. SPX: Real Estate

· Bullish absolute but negative relative scores: XLB, XLE, XLV, XLY, XLP, XLF, and XLU

Table 1: S&P 500 GICS Level 1 Sector ETF Trend Ranks and Scores as of 1/23/2025: Sorted by Tactical Rank

Source: Optuma, Suttmeier Technical Strategies

Historical trend scores over the last 10 weeks

Sector ETF Trend Scores for the last 10 weeks

· Strongest: Seven out of the 11 sectors maximum positive: XLC, XLY, XLE, XLV, XLI, XLB, and XLK

· Weakest: XLRE followed by XLP (at zero)

· Positive over last 10 weeks: XLC, XLY, XLE, XLF, XLV, XLI, XLK, and XLU

· Negative over the last 10 weeks: None – XLP at zero with the potential to shift positive

· Improved last four weeks vs. prior four weeks: XLP, XLE, and XLB

· Deteriorated last four weeks vs. prior four weeks: XLU but XLF’s rank dropped last week

Table 2: Sector ETF Trend Scores for the last 10 weeks

Source: Optuma, Suttmeier Technical Strategies

Sector ETF Trend Scores vs. the S&P 500 for the last 10 weeks

· Strongest: XLK followed by XLV – but XLK has deteriorated as XLV and others have improved

· Weakest: XLF, XLRE, and XLU (all maximum negative) followed by XLC and XLP

· Positive over last 10 weeks: Only XLK but has lost momentum and below its best levels

· Negative over the last 10 weeks: XLC, XLP, XLF, and XLRE

· At zero with the potential for a rotation into positive: XLY, XLE, XLI, and XLB

· Improved last four weeks vs. prior four weeks: XLY, XLP, XLE, XLV, XLI, and XLB

· Deteriorated last four weeks vs. prior four weeks: XLC, XLF, XLK, and XLU

Table 3: Sector ETF Trend Scores relative to the S&P 500 for the last 10 weeks

Source: Optuma, Suttmeier Technical Strategies

Sector ETF Long-term Trend Score for the last 10 weeks

· Strongest: Seven out of the 11 sectors maximum positive: XLC, XLY, XLE, XLV, XLI, XLB, and XLK

· Weakest: XLRE

· Positive over last 10 weeks: XLC, XLY, XLE, XLF, XLV, XLI, XLB, XLK, and XLU

· Negative over the last 10 weeks: None

· Improved last four weeks vs. prior four weeks: XLP, XLE, and XLB

· Deteriorated last four weeks vs. prior four weeks: XLU, but scores for XLF and XLRE dropped last week

Table 4: Sector ETF Long-term Trend Scores for the last 10 weeks

Source: Optuma, Suttmeier Technical Strategies

Sector ETF Trend Long-term Scores vs. the S&P 500 for the last 10 weeks

· Strongest: XLK followed by XLI

· Weakest: XLF, XLRE, and XLU (maximum negative)

· Positive over the last 10 weeks: XLK but has deteriorated from maximum bullish levels

· Negative over the last 10 weeks: XLY, XLP, XLE, XLF, XLV, XLB, XLRE, and XLU

· Improved last four weeks vs. prior four weeks: XLY, XLP, XLE, XLV, XLI, and XLB

· Deteriorated last four weeks vs. prior four weeks: XLC, XLF, XLK, and XLU

Table 5: Sector ETF Long-term Trend Scores relative to the S&P 500 for the last 10 weeks

Source: Optuma, Suttmeier Technical Strategies

Relative rotation graph (RRG)

What is the RRG?

The Relative Rotation Graph (RRG) highlights sector leadership and rotation by plotting relative strength (x-axis) against relative momentum (y-axis) versus a benchmark. This creates four quadrants: Leading (upper right – positive relative strength and relative momentum), Weakening (lower right – positive relative strength and negative relative momentum), Lagging (lower left – negative relative strength and relative momentum), and Improving (upper left – negative relative strength and positive relative momentum). This framework shows the rotation of sectors through different phases of relative performance. Sectors tend to move in the clockwise direction, often crossing through all four quadrants.

Bullish RRG rotation: XLY, XLI, XLC, XLB, XLP, and XLRE as XLF loses momentum

Last week, six sectors — XLY, XLI, XLC, XLB, XLP, and XLRE — showed a positive, up-and-to-the-right heading, indicating improving relative momentum and relative strength. All are in the Improving quadrant with XLY, XLI, and XLB approaching leading. XLC rotated to Improving from Lagging. XLE was flat last week in Improving and just ahead of Leading. All of these sectors except for XLC are in the Improving quadrant, but XLC is pushing toward Improving from Lagging. XLF showed a loss of relative momentum in Improving.

Bearish RRG rotation: XLV and XLU as XLK’s momentum improves

XLU and XLV have down-and-to-the-left headings—signaling deteriorating relative momentum and relative strength. XLU is in Lagging. XLV is in Leading. XLK remains in Weakening after failing to rotate back into Leading in mid to late November but stabilized on improving relative momentum as the sector approaches the Lagging quadrant.

Chart 2: Relative rotation graph (RRG) for the S&P 500 sector ETFs

Source: Optuma, Suttmeier Technical Strategies

Sectors on the move

Financials: Big drop from early January peak pressures key WMA support zone

Financials (XLF) remain in a positive absolute trend, but the zone of the rising 13-, 26-, and 40-week moving averages (WMAs) from 53.83 to 52.61 is under pressure. If XLF breaks these WMAs, it would expose big support at the August and November 2025 lows near 51. A rally back above 53.83-54.11 (13-WMA and last week’s high) is required to confirm the rising 26- and 40-WMAs from 53.42 to 52.61 as support within an ongoing upward trend. If XLF can defend the low 50s as support, then the mid 2025 breakout that projects XLF to 61.25 remains intact.

Chart notes

· Absolute trend scores for XLF have deteriorated from maximum positive levels in the face of maximum negative scores relative to the SPX, which is a challenge for this cyclical sector ETF. See Chart 8 for more.

Chart 3: SPDR Financials Select Sector Fund ETF (XLF): Weekly chart

Source: Optuma, Suttmeier Technical Strategies

Materials: Bullish breakouts point higher toward the 52 and 56 areas

We highlighted the potential for Materials (XLB) to break out above resistance at 46.14-46.43 (61.8% extension and July-September peaks) (December 29, 2025 The Sector Edge). XLB cleared this resistance in early January and pushed to a new all-time high last week. This suggests upside to 51.90-52.07 (converging 100% extensions) and then to 56.30 (late 2024-early 2026 basing pattern count). The immediate trend is bullish above 48 (61.8% extension and last week’s low) with more significant support at the basing pattern breakout zone at 46.43-46.14.

Chart notes

· XLB has had maximum positive absolute trend scores so far in 2026.

· XLB’s relative trend scores have improved since early December as the sector has shown leadership from a multi-year relative low vs. the SPX in late October. Regaining relative price downtrend, chart, and declining 26- and 40-WMAs resistances suggests more enduring leadership for this cyclical sector. The next step: A shift in the Trend Score vs. SPX from zero into positive territory to provide additional bullish confirmation. See Chart 10 for more.

Chart 4: SPDR Materials Select Sector Fund ETF (XLB): Weekly chart

Source: Optuma, Suttmeier Technical Strategies

Energy: Bullish breakout intact above 47.41-46.46 and targets 56.75

Our January 5 The Sector Edge highlighted that Energy (XLE) was in position to break higher from a late 2024 into early 2026 bullish consolidation. The rally above 46.46-47.41 confirmed this positive setup to suggest upside potential beyond the 2024 highs at 48.96-49.49, which XLE is testing, to the mid 2024 peak at 50.76 initially and then higher toward the pattern count at 56.75. Prior resistance at 47.41-46.46 reverses its role to support.

Chart notes

· XLE has had maximum positive absolute trend scores over the last three weeks.

· Although XLE remains below a late 2022 downtrend line vs. the SPX, the sector confirmed a relative double bottom for its October and December 2025 low vs. the SPX. This relative double bottom could precede a push above that downtrend line, especially if the sector’s Trend Score vs. the SPX moves from zero into positive territory to confirm the potential for continued XLE leadership. See Chart 11 for more.

Chart 5: SPDR Energy Select Sector Fund ETF (XLE): Weekly chart

Source: Optuma, Suttmeier Technical Strategies

Utilities: A challenging setup while below 43.53-43.83

Utilities (XLU) have corrected within an uptrend and have traded between rising 26 and 40-week moving averages (WMAs) since early December. While below 43.53-43.83 (13- and 26-WMAs and chart resistance), the risk is for a head and shoulders top. Key support is 41.70-41.15 (late 2024-mid 2025 base breakout/retest zone). If XLU loses this support, it would confirm the topping pattern with deeper risk to 40.26-39.43 (chart support levels and 38.2% retracement). Until a loss of that support, it would take a rally above 43.53-43.83 to reassert the uptrend for XLU.

Chart notes

· XLU has corrected lower on an absolute price basis as absolute trend scores roll over from maximum positive levels and relative trend scores deteriorate to maximum negative levels.

· While XLU remains above key chart, trendline, and WMA support on an absolute basis, the sector broke relative support versus the SPX in late 2025 and reached a new 52-week relative low into early January prior to an uptick. We view this relative weakness as a risk to XLU’s absolute price chart. See Chart 15 for more.

· XLU formed absolute price bullish engulfing pattern as of January 16, but no upside confirmation as 43.53-43.83 resistance is holding so far.

Chart 6: SPDR Utilities Select Sector Fund ETF (XLU): Weekly chart

Source: Optuma, Suttmeier Technical Strategies

Staples: Rallies toward range highs on stealth defensive leadership from October

Staples (XLP) broke above tactical resistance at the declining 26- and 40-week moving averages (WMAs) and chart levels at 79.45-80.25 to confirm an early January weekly bullish engulfing pattern and target the mid 2025-late 2024 peaks at 83.30-84.53 (January 12 The Sector Edge). Prior 80.25-79.45 resistance reverses its role to support. If XLP remains above this support, the potential increases for a breakout beyond the 2024-2025 peaks that would favor continued upside to 87.11 (61.8% extension) and 94.51 (100% extension).

Chart notes

· Prior 80.25-79.45 resistance reverses its role to support ahead of rising 200-WMA and range lows, which offer additional support at 76.35-75.16.

· Absolute price scores up ticked to their best levels since mid September to confirm the breakout above the 79-80 area. A shift from zero to a positive Trend Score would offer addition confirmation, increasing the potential for new all-time absolute price highs on XLP.

· The last multi-year relative low for this defensive sector occurred in late October. Since then, XLP has shown stealth leadership within its long-term lagging trend vs. the SPX. See Chart 16 for more.

Chart 7: SPDR Staples Select Sector Fund ETF (XLP): Weekly chart

Source: Optuma, Suttmeier Technical Strategies

S&P 500 GICs 1 “cyclical” sector ETF charts

Financials: Absolute scores drop as XLF remains maximum negative vs. SPX

Financials (XLF) remain in a positive absolute trend, but the zone of the rising 13-, 26-, and 40-WMAs from 53.83 to 52.61 is under pressure as absolute trend scores deteriorate from maximum positive levels in the face of maximum negative scores relative to the SPX. If XLF breaks these WMAs, it would expose big support at the August and November 2025 lows near 51. A rally back above 53.83-54.11 (13-WMA and last week’s high) is required to confirm the rising 26- and 40-WMAs from 53.42 to 52.61 as support within an ongoing upward trend.

Chart 8: Financials (XLF) and XLF vs. SPX (top), Trend Scores (center), and Long-term Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Industrials: Bullish absolute trend and watching resistance vs. the SPX

The Industrials sector (XLI) reached a new weekly closing basis record high in mid January on maximum positive absolute trend scores. Relative trend scores vs. the SPX have improved with the long-term score shifting to positive. As a next step, we are on alert for a breakout above key relative chart and downtrend resistance that would confirm a 3-year bottom for XLI vs. the SPX and a shift in the Trend Score vs. SPX from zero into positive territory to suggest more enduring leadership for this cyclical sector.

Chart 9: Industrials (XLI) and XLI vs. SPX (top), Trend Scores (center), and Long-term Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Materials: New all-time highs and a push above key resistance vs. the SPX

After defending its rising 200-week moving average and shifting to positive absolute price trend scores (Nov 3 and Oct 20 The Sector Edge), Materials (XLB) achieved an upside breakout (Dec 29 The Sector Edge) and went on to an all-time high last week. In addition, XLB’s relative trend scores have improved as the sector has shown leadership from a multi-year relative low vs. the SPX in late October. Regaining relative price downtrend, chart, and declining 26- and 40-WMAs resistances suggests more enduring leadership for this cyclical sector. The next step: A shift in the Trend Score vs. SPX from zero into positive territory to provide additional bullish confirmation.

Chart 10: Materials (XLB) and XLB vs. SPX (top), Trend Scores (center), and Long-term Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Energy: Probes to new high after bullish breakout and double bottom vs. SPX

After dropping to a marginal multi-year low vs. the SPX in late December, Energy (XLE) has rallied on both an absolute and relative price basis into early 2026, breaking absolute downtrend resistance, confirming a double bottom vs. the SPX, and reaching a 52-week high last week. Although XLE remains below a late 2022 downtrend line vs. the SPX, this relative double bottom could precede a push above that trend line, especially if the Trend Score vs. the SPX moves from zero into positive territory to confirm the potential for continued XLE leadership.

Chart 11: Energy (XLE) and XLE vs. SPX (top), Trend Scores (center), and Long-term Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

S&P 500 GICs 1 “growth” sector ETF charts

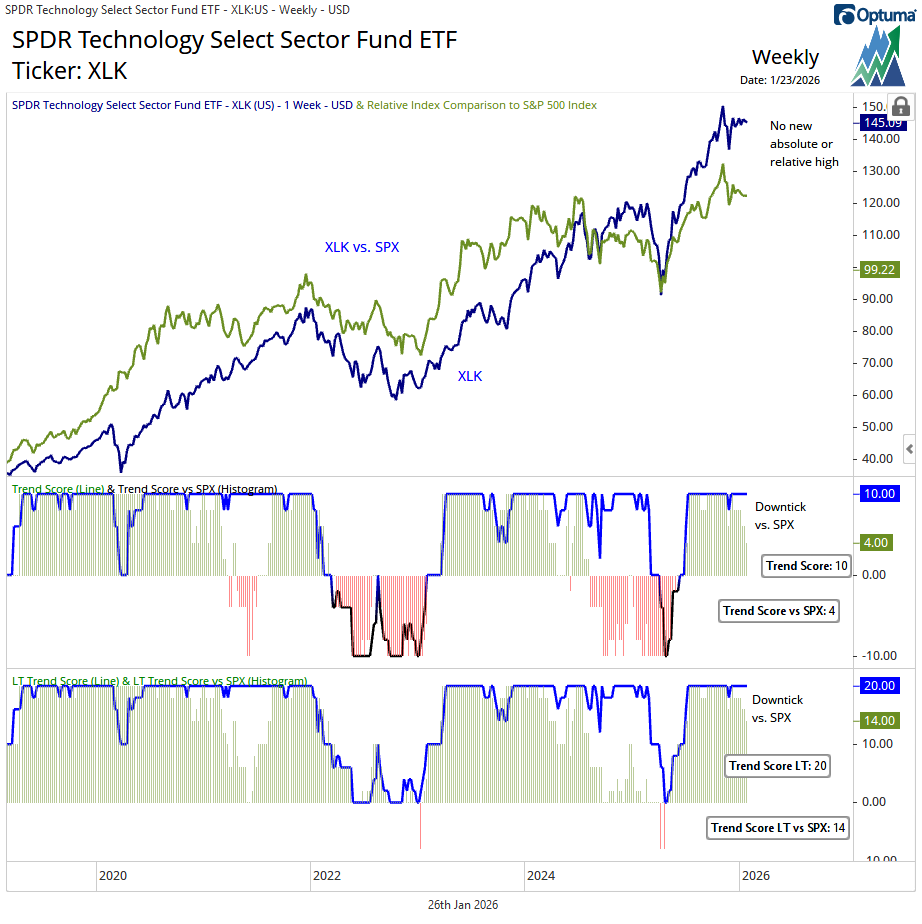

Technology: Lost momentum and consolidates within positive trends

Technology (XLK) has lost momentum. The sector last achieved absolute and relative price basis 52-week highs in late October and has since consolidated within bullish absolute and relative price trends as defined by rising 26- and 40-WMAs. Although XLK has struggled on an absolute basis since its early November weekly upside exhaustion gap and bearish engulfing pattern (Jan 5 and Dec 22 The Sector Edge), weekly closes above the rising 13-WMA (144.67) have kept the absolute trend scores at maximum positive levels since late November even as XLK has deteriorated vs. the SPX and retests its September breakout point and rising 26-WMA relative to the SPX.

Chart 12: Technology (XLK) and XLK vs. SPX (top), Trend Scores (center), and Long-term Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Discretionary: Maximum positive absolute, but choppy scores vs. SPX

Discretionary (XLY) has had maximum positive absolute trend scores since late November that increase confidence in the sector’s breakout from a late 2024-late 2025 bullish cup and handle (Dec 1 The Sector Edge). New absolute price highs in early January offered additional confirmation. While the potential for a late-2022 to late-2025 head-and-shoulders bottom (H&S) versus the SPX remains intact, XLY must reclaim all of its weekly relative price moving averages and improve its Trend Score vs. SPX from zero into positive territory to bolster the case for this H&S bottoming pattern (Dec 22 and Oct 6 The Sector Edge).

Chart 13: Discretionary (XLY) and XLY vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Comm Services: Stalls after bull flag breakout and struggles vs. SPX

Although absolute trend scores remain solid and Communication Services (XLC)’s early December bullish flag breakout remains intact (Dec 8, Dec 1, and Nov 10 The Sector Edge), the sector is struggling relative to the SPX. The Trend Score vs. SPX hit has been at or near maximum bearish levels so far in 2026, and it would take strength above the 13-, 26-, 40-WMAs for XLC vs. the SPX to improve the Trend Score vs. SPX. The Long-term Trend Score vs. SPX has held the zero level and is underpinned by a rising 200-week moving average vs. the SPX.

Chart 14: Comm Services (XLC) and XLC vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

S&P 500 GICs 1 “defensive” sector ETF charts

Utilities: Corrects within bullish absolute trend but maximum negative vs. SPX

Utilities (XLU) have corrected lower on an absolute price basis as absolute trend scores roll over from maximum positive levels and relative trend scores deteriorate to maximum negative levels. While XLU remains above key chart, trendline, and weekly moving-average support on an absolute basis, the sector broke relative support versus the SPX in late 2025 and reached a new 52-week relative low into early January prior to an uptick. We view this relative weakness as a risk to XLU’s absolute price chart.

Chart 15: Utilities (XLU) and XLU vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Staples: Absolute strength on stealth leadership vs. SPX since last October

Staples (XLP) continued to rally last week on leadership vs. the SPX and broke above downtrend resistance from late 2024 to place the focus on the 2024 peaks. Absolute price scores up ticked to their best levels since mid September to confirm this move (Jan 12 The Sector Edge) and a shift from zero to a positive Trend Score would offer addition confirmation, increasing the potential for new all-time absolute price highs. The last multi-year relative low for this defensive sector occurred in late October, and XLP has shown stealth leadership within its long-term lagging trend since then.

Chart 16: Staples (XLP) and XLP vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Real Estate: Choppy and negative absolute scores and firmly bearish vs. SPX

We continue to monitor a potential base-building process for Real Estate (XLRE) from mid 2022 (Oct 20 and Sep 29 The Sector Edge) but need a sustained improvement in absolute and relative trend scores for any confidence in this pattern. Tactical absolute and relative strength have stalled. Absolute trend scores remain choppy in negative territory, as relative scores have remained at or near maximum negative since late May 2025.

Chart 17: Real Estate (XLRE) and XLRE vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Healthcare: Constructive and watching absolute and relative price resistances

Healthcare (XLV) has stalled at resistance on both an absolute and relative price basis, but the sector has maximum positive absolute price scores and improving scores relative to the SPX. This suggests that XLV is consolidating within improving absolute and relative price trends and could see renewed upside to absolute price highs above the late 2024 and late 2025 peaks and the potential for continued leadership vs. the SPX beyond and relative chart and downtrend resistance.

Chart 18: Healthcare (XLV) and XLV vs. SPX (top), Trend Scores (center), and LT Trend Scores (bottom)

Source: Optuma, Suttmeier Technical Strategies

Suttmeier Technical Strategies, LLC (STS) provides financial commentary and market analysis for educational and informational purposes only. We are not registered investment advisors, and nothing published by STS should be considered personalized investment advice, a recommendation to buy or sell any security, or a solicitation to engage in investment activity. All content is impersonal and does not consider your individual financial circumstances. Past performance is not indicative of future results. Investing involves risk, and you should consult with a licensed financial advisor before making any investment decisions. STS or its representatives may hold positions in securities mentioned in our publications. Such holdings are subject to change without notice and do not constitute investment advice.

Comments